When you buy a home, you are making a large financial decision. You will need to make a long-term financial commitment to pay a home loan. And your success in repaying your home loan largely depends your loan repayment plan, which includes the loan tenure and the other costs of owning your home.

Deciding on your loan tenure is important, as it determines the size of the loan amount. The longer your loan, the larger your interest payment. Banks usually grant a loan tenure for up to 30 to 35 years, depending on your age.

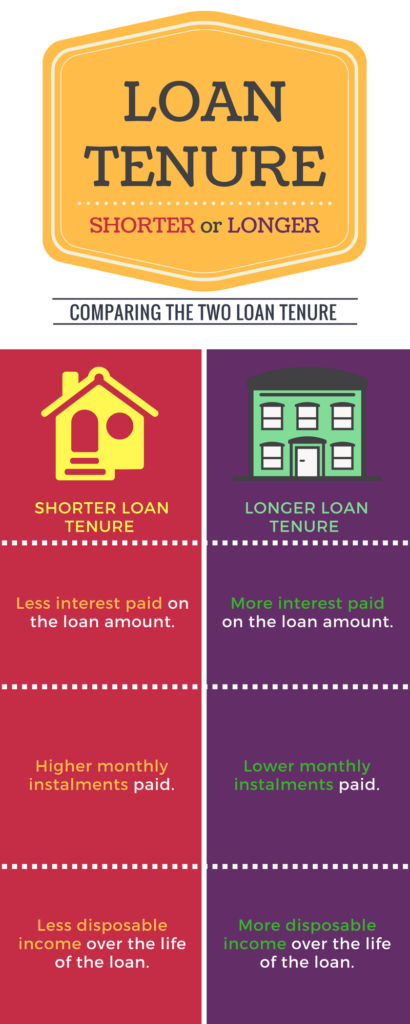

Comparing Home Loan Tenure

The diagram below summarizes the three main differences of the shorter loan tenure and the longer loan tenure:

- The length of the loan tenure affects your total financial commitment.The shorter your loan tenure, the lower your total financial commitment. When you take a home loan, you are committing to pay the principal and interest on the loan. The shorter your loan tenure, you pay a lower interest on your loan amount. Thus, reducing your total financial commitment to service the loan.

- The length of the loan tenure affects your monthly payments. The shorter your loan tenure, the higher your monthly financial commitment. However, you should never overlook your other monthly costs related to home ownership, such as home insurance, mortgage insurance, property taxes, utility bills, or even credit card bills (if your furnishings were bought using credit). These costs may creep up on you unknowingly, affecting your lifestyle; which lead us to our next point.

- The length of the loan tenure affects your monthly cash flow.The shorter your loan tenure, the lower your disposable income during the life of the loan. When you decide to aggressively pay the loan on a shorter loan tenure and at much steeper monthly payments, you may think that this would cut your loan payment short and clear your interest payment. However, you may find yourself in a very tight monthly cash flow situation.

Other Factors to Consider

There are two other factors you would need to consider before deciding your loan tenure. The first factor is risk. Banks typically offer two types of home loans:

- Fixed rate home loan packages where a fixed rate will apply for an initial period before floating rates apply; and,

- Floating (or variable) home loan packages where interests are determined by a reference interest rate.

When you choose a shorter loan tenure, spikes in interest rates may affect your monthly payments. This may increase your monthly loan payment significantly for the short term. A longer loan tenure, however, would provide you some comfort from such spikes. Thus, a longer loan tenure reduces your risk to spikes in your home loan payment.

The second factor to consider is the banks’ refinancing policies. You may have good reasons to pay off your debt as quickly as you can, but if you encounter difficulties keeping up with the higher monthly instalments, and would like to extend your loan tenure, it may not be so easy, if at all possible. Most banks have a policy where borrowers will only be allowed to take over the remaining loan tenure at a point of refinancing.This move may force you to lower your loan tenure and increase your monthly payment instead.

The banks’ refinancing policies usually favour the longer loan tenure. If you, by chance, have a windfall and would like to shorten your loan, banks would impose penalties for paying down (or off) you loan early.

Ultimately, choosing your home loan tenure would require that you balance both your short-term and long-term financial needs. And, if you know your circumstances and your financial goals clearly, owning your home would not be such a headache.